Data Sources

This study used Citeline’s Trialtrove database to obtain data on the number of clinical trials initiated between 7/2014 and 8/2024. Citeline’s Trialtrove database comprehensively covers registered drug trials, providing detailed and manually curated trial information. In the main analysis, we included post-approval Phase I-III trials that were primarily sponsored by industry, excluding trials for all vaccines and therapeutics for the prevention and treatment of COVID-19 infections. Government-funded trials were identified using the same inclusion and exclusion criteria for comparison, but required post-approval Phase I-III trials that were primarily sponsored by the government. Data were extracted in 01/2025.

Study Design

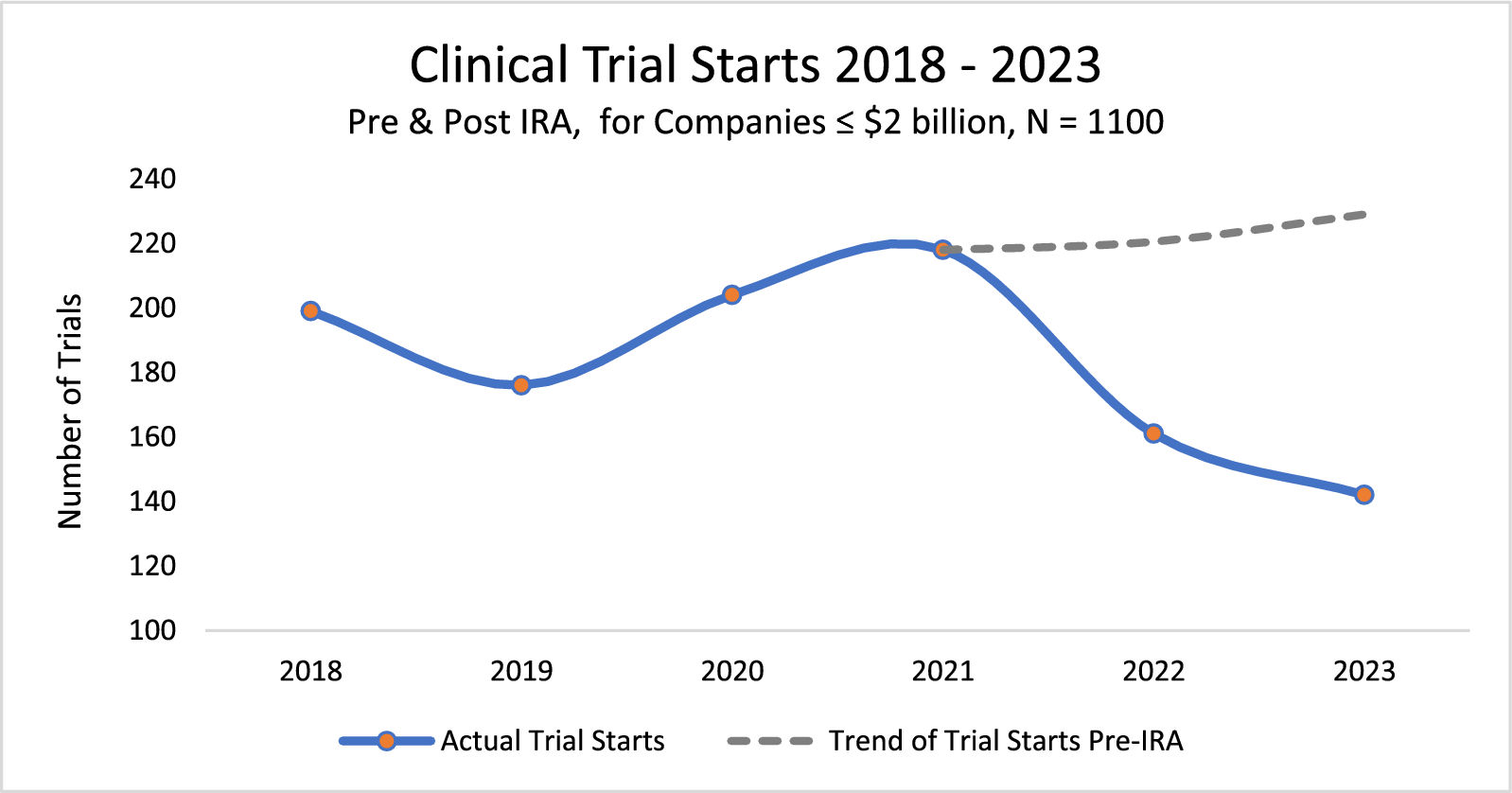

In this longitudinal study, we used interrupted time series analysis (ITSA) to estimate the impact of the passage of the IRA on post-approval clinical development with an aggregated monthly number of trials as the outcome measure. ITSA is a quasi-experimental design broadly used in public health and policy analysis to examine the impact of non-randomized interventions [12]. With the IRA passage in 8/2022 serving as the intervention, we defined the pre-IRA period as 7/2014-7/2022, and the post-IRA period as 8/2022-8/2024. Our analysis compared the level (i.e., number of trials) and trend (i.e., number of trials/month) in post-approval Phase I-III clinical trial initiation during the pre- and post-IRA periods to estimate the impact of the IRA’s passage. To further quantify the potential impact of the IRA, we used the pre-IRA trend estimated from the ITSA model to project the expected number of monthly industry-funded trials at the end of the observation period (8/2024), assuming the IRA had not been passed. This projection was then compared with the actual observation and the predicted trial count in 8/2024 based on the full ITSA model that incorporated the IRA-related level and slope changes, respectively. Note the projection may be a conservative one as the pre-IRA decline likely primarily reflects temporary disruptions due to the COVID-pandemic, which may have gradually resolved over time.

For comparison, we conducted an additional ITSA to examine changes in government-funded trials post-IRA. Government-funded trials were selected as a comparator as they were hypothesized to be unaffected by the IRA but sensitive to other potentially confounding, external changes in the clinical development environment, such as shifts in public health priorities, the COVID-19 pandemic, and technological advancements [13].

Scenario Analyses in Industry- and Government-Funded Trials

In addition to the base-case ITSA, a series of scenario analyses across both industry- and government-funded trials were conducted to test the robustness of our findings. First, past research suggests that threats of pharmaceutical price regulation have had negative impacts on firm-level research and development even when proposed legislation has not become law [14]. Accordingly, recognizing that the effects of the IRA may have begun even before its official passage, we conducted an ITSA modeling the event to start in 11/2021, when the United States House of Representatives first proceeded with debate on the IRA (Scenario 1) [1].

Second, recent research suggests that the COVID-19 pandemic was associated with delayed clinical trial enrollment and timelines [13]. Because our base-case ITSA included time periods before, during, and after the pandemic, we conducted a scenario analysis limiting the time horizon of the ITSA to a period after the pandemic had begun. Specifically, we ran the ITSA from 1/2020 to 8/2024, such that the pre-IRA period (1/2020-7/2022) excluded pre-pandemic clinical trial environment while still capturing potential impacts of COVID-19 on clinical trial initiation in the pre-IRA period (Scenario 2).

Finally, as a supporting analysis, we ran a difference-in-difference model (DiD) by comparing the changes in industry-funded trials before and after the IRA passage (first difference) with those of government-funded trials (second difference), which served as a counterfactual. The underlying assumption was that trials would have changed similarly in the two groups in the absence of the IRA. The DiD model more directly compares industry- and government-funded trials by comparing whether the two groups changed in the same amount and direction around the interruption (i.e., IRA’s passage). However, unlike the ITSA, this model cannot answer questions about the magnitude of the level or trend change following the interruption, and therefore among other limitations the DiD was used as a secondary and supporting analysis.

Sensitivity Analyses Within Industry-Funded Trials

Beyond the use of government-funded trials as a comparator (ITSA) and counterfactual (DiD) to control for potentially confounding changes during the study period, we conducted further sensitivity analyses to (1) explore the degree to which specific exogenous factors may have impacted industry-funded trials over time and/or the face validity of the base-case ITSA results, and (2) examine whether the impact of the IRA differed by type of drug (small vs. large molecule) and across selected therapeutic areas.

First, the Federal Reserve increased interest rates 11 times from March 2022 to July 2023 [15]. Smaller and earlier-stage biotechnology companies may be more sensitive to both rising and falling interest rates given their impact on net present value models and company valuation [16, 17]. Accordingly, we explored changes in pre-/post-IRA trial initiation in two subgroups of industry sponsors: top 20 and non-top 20 pharmaceutical companies (identified by Citeline based on overall R&D activity and market presence). The goal of this subgroup analysis was to explore the degree to which financial environment changes may have confounded our estimates of the IRA’s effect. We hypothesized that large pharmaceutical firms would be less sensitive in the short run to the interest rate increases occurring amidst IRA passage when compared to smaller biotechnology firms; that is, we hypothesized that large pharmaceutical firms would have lower relative changes in trial investments due to increased interest rates. Notably, potential differences in IRA impact between large pharmaceutical firms and smaller biotechnology firms may have reflected not only differential interest rate sensitivity but also anecdotal evidence that venture capital (VC) investors of biotechnology firms and their limited partners (LPs) may exhibit an increased risk aversion during the IRA period, leading to decreases in new capital [10].

Second, it was hypothesized that significant shifts in the therapeutic market-basket dynamics (e.g., sudden increase the number of drugs going off-patent) may have impacted overall trends in the initiation of new clinical trials in post-approval drugs. We obtained and described data from the U.S. Food and Drug Administration on the number of first-approved generics from 2014 to 2023 (2024 data unavailable) to identify any significant shifts in the volume of generic entry over the study period.

Additionally, the IRA introduced distinct timelines for small and large-molecule drugs to become eligible for price negotiation, which others have described as creating a “pill penalty” disincentivizing initial and ongoing clinical development for small molecule drugs [18]. We described pre-/post-IRA changes in small molecule vs. large-molecule drugs to explore potential differences in the impact of the IRA on post-approval clinical development given the differential timeline towards DPNP eligibility. Finally, we analyzed changes in the number of post-approval trials following the IRA in the five largest therapeutic areas, as defined based on the volume of trials in Citeline: oncology, autoimmune/inflammation, central nervous system, metabolic/endocrinology, and cardiovascular diseases. Trials assigned to multiple therapeutic areas were excluded from this subgroup analysis to avoid potential double counting and classification ambiguity.

Statistical Approach

Descriptive statistics were applied to summarize the monthly average of newly initiated trials before and after IRA passage across the entire study period, and in a more targeted time from the year prior to IRA passage to the most recently available year. In the ITSA, a linear regression was conducted to evaluate IRA-related changes in level (i.e., immediate shift following the IRA’s passage) and slope (i.e., monthly change in trial initiations compared to the estimated counterfactual without the IRA). Although autocorrelation was not detected, we used Newey-West robust standard errors to enhance the reliability of the estimate. The DiD model was fit using a linear regression, incorporating an indicator of industry- vs. government-funded trials and time indicator to account for time-invariant differences and secular trends unrelated to IRA’s passage. Based on both statistical and visual inspection of the parallel trend assumption, the pre-IRA period for the DiD analysis was defined as 1/2020 to 7/2022. Wilcoxon rank sum test was used to assess whether differences in trial initiation were statistically significant after IRA’s passage in the subgroup analyses of (1) top 20 companies vs. non-top 20 companies, (2) small-molecule vs. large-molecule drugs, and (3) five largest therapeutic areas.

Comments (0)