This nationwide study provides an extensive analysis of the ETN price evolution in an off-patent market, covering all RMD drug purchases by the public payer. This real-life scenario demonstrates how re-monopolization, even by a biosimilar, rapidly increases healthcare expenditure, which has negative downstream effects on hospital funds and may lead to treatment restriction for patients, while also reversing the cost reduction previously derived through competition due to biosimilar market introduction. In the Polish case, the root cause of market re-monopolization was the regulator's decision to maintain only one biosimilar drug on market. This was achieved by withdrawal of reference drug reimbursement, with an underlying, illusory belief that the biosimilar drug would not become more expensive.

Access to biologics varies across Europe and is based on the funding of healthcare systems [18, 19]. The initially high prices of biologics have led to regulatory restrictions, such as stringent disease activity thresholds or prior, multiple csDMARD failure. In some countries, entry criteria have relaxed following biosimilar introduction [6, 20]. In Poland, despite reductions in therapy costs [5, 10], regulations have only modestly improved [13].

The number of RMD patients treated with ETN in Poland has substantially increased over a 10-year period [10]. However, the growth rate was not incremental throughout the biosimilar era. The decrease in annual cost of ETN therapy was marked, but still smaller when compared to ADA and INF [5]. Within this study, the total volume of ETN corresponds to 12,573 patient-years of treatment during the competitive period and 3942 patient-years during re-monopoly. The lowest average price from winning tenders throughout the competition period ranged between €7.28 and €9.48. During this time, the highest mean price (€9.48 for Benepali) was derived from one biosimilar drug being available only for a limited time. Later on, even under competition of two drugs, lower prices were maintained in tenders. Importantly, the average prices for the competition period do not fully reflect financial benefits, as they include higher prices from the initial period. We also observed that achieving a lower price at a given time under stable competition is sustainable. This is reflected in the average winning offer price from the last 6 months of competition, which can be treated as a measure of cost reductions (€5.69). Interestingly, during this time, the lowest price was offered by the reference manufacturer (€5.15). This illustrates that repricing of the reference drug is possible and allows for effective market competition with biosimilars. Despite rheumatology dominance with the ETN market (> 99%), individual tenders in dermatology remain insightful. For tenders won by both the reference drug and the biosimilar, the price was significantly lower than in the RMD sector (€5.51–6.34). Of interest, in one dermatology tender, even without a bid from the reference manufacturer, mere awareness of competition stimulated a low bid price. In 2021, the market share of reference ETN in Poland was ~30%, while that of the other less costly TNFis (ADA and INF) was near null [5]. In contrast, reference ADA and INF manufacturers were unable to compete on the market, though low prices were still maintained due to ongoing competition between biosimilars. In Scandinavian countries, in successive years, both biosimilar drugs (SB4 or GP2015) and the reference drug ETN (Enbrel) have won centralized tenders, demonstrating the potential of price shaping by the reference drug [6, 21].

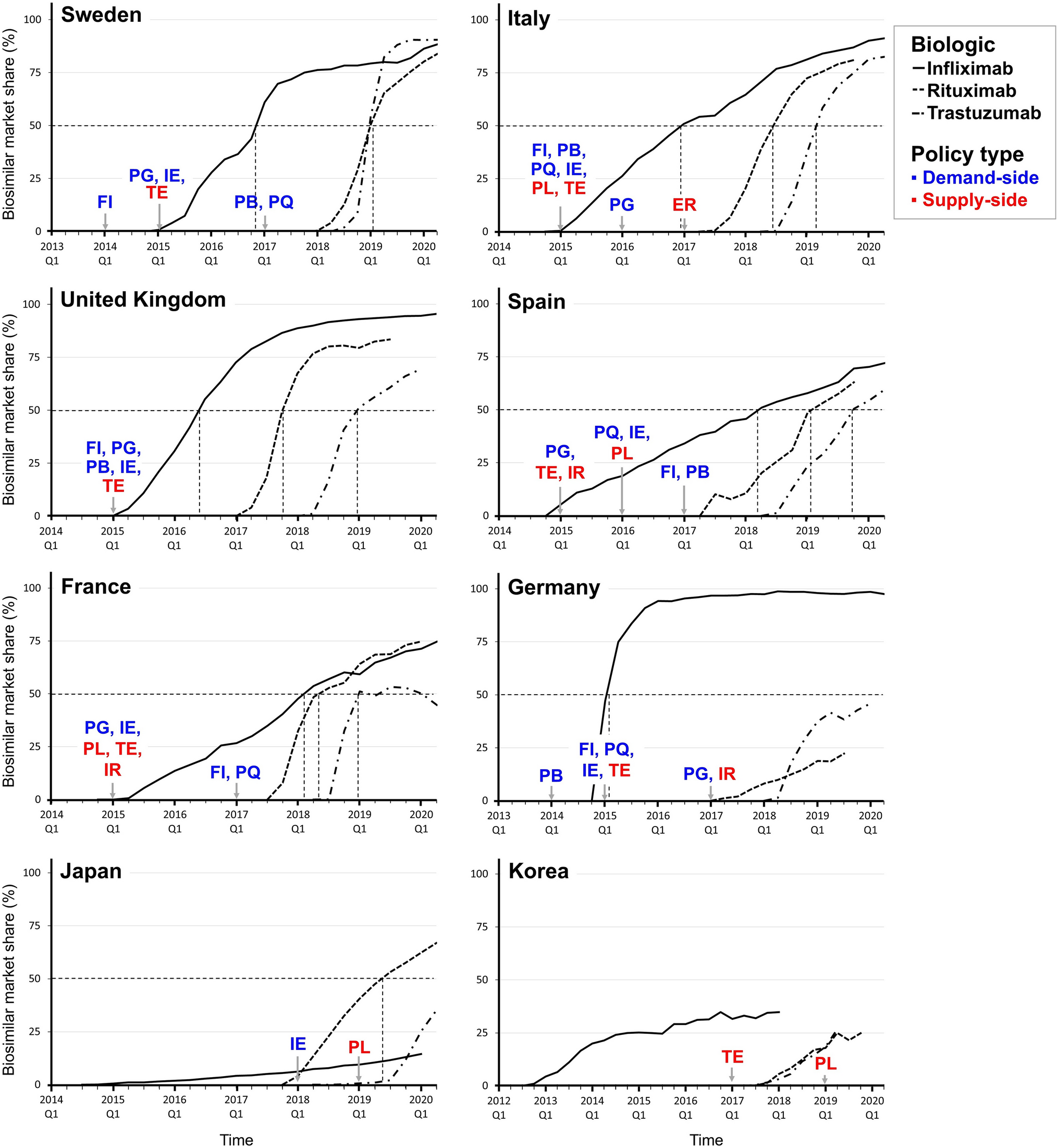

In Europe, the ratio of biosimilar to reference drug users varies, often changing over time in favor of biosimilars [22,23,24,25,26,27,28]. This trend is most pronounced in countries where substitution is mandatory, and determined by tenders. For local tenders, more entities can consistently compete for market share at a given time. However, in centralized tenders, in countries where a single-winner policy applied, only one manufacturer's drug is designated for use at any given time. Our results are in line with other studies that demonstrate all forms of competition ensure market stability and contribute to consistent price reduction [29].

In countries where biosimilar or reference drug use is obligatory and fixed in a tender, various approaches for introducing a new agent exist [19, 21, 29, 30]. Regional- and nation-wide strategies include a mandate of the selected agent for all or only for new patients. Strategies of switching also vary, while algorithms often require downward pricing under a given threshold. It should be noted that all such procedures often entail additional healthcare service costs [21, 31]. In Poland, switching drugs is mandatory regardless of disease activity or difference in drug prices. Patients receive the new agent at their next scheduled appointment, which ensures use of the tender-winning drug in every case, even if its most recent price has increased. Reimbursement remains predicated on the winning price not exceeding the upper financing threshold. However, the list price (financing limit) is often significantly higher than prices obtained in local (hospital) tenders during competitive periods [13], making it feasible to markedly increase the drug price for hospitals in the absence of competition.

No prior studies have described cost evolution in the scenario of a biosimilar remaining as the only drug in an off-patent market. We recorded that under ETN biosimilar monopoly, the average price increased up to €8.09 over the whole timeframe, including a higher increment in the last 6 months (up to €9.71). When comparing monopoly and competition periods, this corresponds to an increase of about 40–70%. Most recent ETN prices have tripled compared with the lowest competitive prices (and were near equal to the upper financing limit) and exceeded the winning offers from the initial broad market period (~ November 2017). Taken together, the annual treatment cost (gross) per patient (based on the last 6 months of monopoly average price) was estimated at €3828, thus exceeding the cost of treatment in 2018. Moreover, when comparing with the highest price that emerged in recent tenders (resultant estimate of €6236), the projected costs exceed those from early 2017. Under current regulations, these price projections are likely to be sustained in the absence of competition.

During the competitive period, we observed a significant relationship between tender volume and winning price, which was not recorded during re-monopoly. Once achieved, higher pricing remains constant and irreversible, with a sudden increase over time, regardless of order size. These data support observations from other countries, where it has been shown that the ability to generate savings is mainly derived from competition [18, 19, 29]. There is also a positive relationship between the saving size and the number of tender competitors, but a negative association with time lag since the drug equivalent entered the market [32]. In our analysis, the possibility of competition among three drugs existed for a limited time, though no marked difference in winning prices could be observed when bids were submitted by two or three manufacturers. This was also observed during a period when the decrease in the price of ETN was reactive.

Tenders settled during the monopoly period have a delayed impact on current projections for ETN reimbursement. Data from the public payer covering the monthly drug cost from January 2018 to December 2023 supports the trend observed in tenders. The average reimbursement cost in June 2022 was €5.68 (ETN DDD, net), reaching its lowest value in November 2022 (€5.58). From the following month, the reimbursement cost steadily increased, reaching €7.46 in December 2023, i.e., the level that was last seen in February 2021. Differences in reimbursement costs published by the NHF (compared to biosimilar tender prices) during re-monopoly stem from continued implementation of contracts concluded during the competitive period. This will likely result in attenuation of expected drug price increases in subsequent months, as we have yet to observe an obvious change in pricing over the most recent tenders.

With biologics nearly entirely funded by the public payer in Poland, the increase in drug prices has direct economic consequences. The loss incurred by the NHF during the period of re-monopoly amounts to almost €3.5 million. However, the net effect of the increasing treatment cost may be lower, in part due to reduced expenditures for healthcare services. In order to encourage wider uptake of biosimilars, various countries are implementing different incentive systems [19, 33,34,35,36]. Studies from various European countries, including Poland, show that the share of off-patent drugs is steadily decreasing, at the expense of more modern on-patent therapies [10, 21, 22, 30]. While selecting the cheapest drug from the off-patent group guarantees its market share, there is no priority over other on-patent drugs, often with different modes of action. Even under comparable efficacy and safety, the physician may decide to choose the more expensive therapy. Therefore, for the patients’ benefit, tangible and non-tangible incentives [37, 38] appear essential to realize the true potential of biosimilars, i.e., effectively treating a greater number of patients under a similar budget [39, 40].

In Poland, the financial incentive strategy is based on higher valuation of healthcare services in hospitals that purchase drugs under NHF-set thresholds (not list price). Consequently, an increase in ETN prices that exceeeds the NHF limits also restricts additional sources of hospital income. We estimate that if all tenders during re-monopolization resulted in a price allowing for favorable financing, hospital gains could theoretically amount to €1.89–2.52 million (overall). The resultant loss for hospitals represents relative cost savings for the public payer. Consequently, the NHF partially covers the costs incurred due to higher priced therapy, but may also result in patients’ limited access to hospitals providing biological treatment.

If maintenance of high pricing continues in Poland, RMD costs may markedly escalate with the rising number of incident cases. ETN prices also affect increases cumulatively in hospital finances, which in case of fixed-funding limits, are likely to restrict the number of services rendered (and thus the number of patients treated). In addition, reduction of the ETN market share may destabilize the local market, ultimately leading to ETN shortages. The present setting in RMDs may prove even more restrictive than the early biologic era. We previously reported that despite the less costly TNFis being widely prevalent in clinical practice, their market share in Poland has consistently declined [10], despite the presence of incentivization strategies, the failure of which has also been reported in other European countries [33]. Communication and countermeasure strategies are likely the main solutions for the Polish dilemma. Policy changes should be discussed with all key stakeholders, while financial incentives should be re-designed, in order to achieve the potential advantages attributed to affordable biologics, while keeping in mind the economic laws of market behavior. On both a provider and a patient level, appropriate educational programs should be encouraged (e.g., regarding effectiveness and safety of less costly biologics). In summary, the maintenance of a healthy market should ideally be regulated with ongoing input from the pharmaceutical, financial, and medical sectors, to provide long-term sustainability and competitiveness [41, 42]. Finally, on a local level, transfering reimbursement (from hospital-based) to the outpatient and pharmacy setting appears to be a crucial factor for increasing biologic availability in Poland.

Comments (0)